South India — Tamil Nadu, Kerala, Karnataka, Andhra Pradesh, Telangana — is no longer just a regional market. It’s a high-growth economic zone with distinct consumer behaviour patterns. What works in North India doesn’t always work here. And that’s exactly where market research becomes powerful.

South India is staging one of the most significant consumer market transformations in the country. Brands winning here aren’t copy-pasting their north Indian playbooks — they’re winning because they chose to understand this market on its own terms, through research, data, and genuine cultural curiosity. This piece breaks down what’s really happening in the South Indian market, why standard assumptions break down here, and how market research becomes the single most important investment a brand can make in this region.

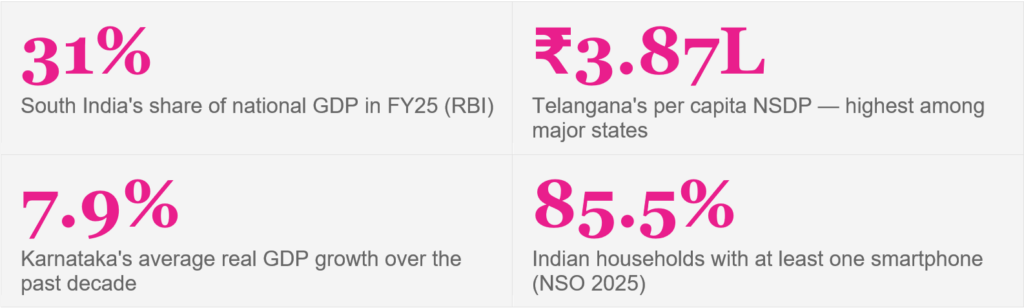

The numbers don't lie: South India is a growth engine

The five southern states contribute approximately 31% of national GDP in FY25 — ahead of the North at 30% — despite accounting for just 20% of the population. The per capita income story is even more telling.

All five states rank in India’s top 10 for per capita income. Telangana leads at ₹3.87 lakh, followed by Karnataka at ₹3.80 lakh, Tamil Nadu at ₹3.61 lakh, Kerala at ₹3.08 lakh, and Andhra Pradesh at ₹2.66 lakh. Karnataka recorded the highest decade-long real GDP growth at 7.9%, followed by Telangana at 7.1%. On the digital side, 85.5% of Indian households now own a smartphone, with South India consistently outperforming the national average.

These aren’t abstract figures. They represent real purchase intent, changing media habits, and an increasingly sophisticated consumer who will not respond to a generic pan-India playbook.